High Yield: Positioning for Tariff-Induced Turbulence

High yield bonds and loans remain fundamentally sound, with attractive breakevens and a solid margin of safety against default losses. With further volatility likely, we expect both challenges and opportunities to emerge.

If the last few weeks have taught us anything, it’s that volatility is likely here to stay.

High yield bonds and loans felt the effects of this in the immediate aftermath of the Trump administration’s tariff announcement, with spreads widening and month-to-date returns turning negative. The market has since retraced much of that ground following the abrupt suspension of most tariffs for 90 days, which also reduced immediate downside risks and lowered the odds of a protracted selloff in the asset class.

Although market sentiment has clearly improved, the recent announcements likely mark the starting point for negotiations rather than the end point—meaning the uncertainty around U.S. trade policy and its potential effect on global growth and inflation will almost certainly persist. And if history is any guide, financial markets—including high yield—will continue to react (and maybe overreact) to both positive and negative headlines going forward. However, while bouts of volatility can be challenging to navigate, they arguably, and perhaps counterintuitively, can also lead to select opportunities and very attractive entry points.

Fundamental Margin of Safety

Supporting this view, high yield bonds and loans remain reasonably well positioned to navigate the current environment. From a fundamental standpoint, credit metrics broadly are starting from very healthy levels—a reflection of several years of conservative behavior on the part of high yield issuers. Net leverage on average came into the year at comfortable levels at 3.4x in the U.S. and 3.1x in Europe for the high yield bond market, and at 4.0x for the U.S. loan market. Similarly, while deteriorating slightly from peak levels in 2022, interest coverage remains solid at 4.2x in the U.S. and 5.1x for Europe for high yield bonds, and at 4.0x for U.S. loans.1

Of course, certain sectors of the market are more inherently exposed to tariffs than others. Companies in consumer products, retail, manufacturing and automotive sectors may face greater challenges, for example, especially those that have a manufacturing footprint in jurisdictions within the scope of the tariffs. Even for the more exposed companies, however, the impact is likely to be nuanced, as certain companies may have the ability to shift production and/or pass through some or all of the financial impact on pricing to their end consumers. For sectors and companies with larger domestic footprints, the impact will likely be relatively benign.

How About Defaults?

Setting risk premia and rate volatility aside, the biggest fundamental risk to bond and loan market returns comes from the potential for default losses. While the path ahead is uncertain and subject to change, there are several reasons why we are not overly concerned about default losses over the next 12 months. For context, the trailing 12-month default rate across global high yield markets ranges from less than 1% to 3%, depending on the region and market. Given the combination of a solid fundamental starting point, the higher quality profile of the global high yield bond market—56% of which is rated double-B—and limited near-term maturities, particularly in the loan market, we believe it is unlikely that defaults will increase significantly this year.2

Additionally, elevated yield levels of approximately 8% to 9% provide a cushion to mitigate the impact of temporary price disruptions and unexpected default situations.3 Further, many default situations are identified well in advance, allowing them to be considered in portfolio positioning, with potential outcomes already reflected in trading levels. Therefore, while the current environment certainly warrants caution, we do not believe default losses will be a significant headwind for performance in high yield markets.

Attractive Breakevens

In terms of performance going forward, the combination of high all-in-yields (near 8%) and short duration (less than 3 years) that characterize the high yield bond market today should help mitigate the impact that spread widening has on total returns.4 If yields remain in their current range, spreads—which between 400 and 500 basis points (bps)—would need to widen by over 250 bps before investors would experience a negative return over a 12-month period.

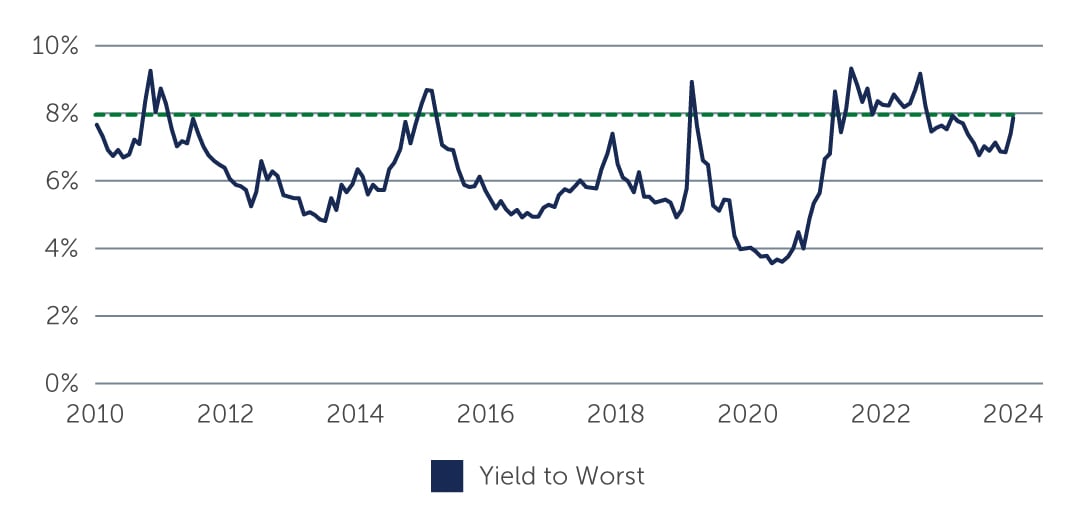

Additionally, a 250+ bps increase in the yield-to-worst would imply all-in-yields of ~11%, which is a level not typically seen outside of recessions. In fact, in nearly all the major high yield market sell-offs—2008/2009 (Global Financial Crisis), 2011 (Sovereign Debt Crisis), 2015 (Commodity Downturn), 2020 (Covid) and 2022 (Rising Interest Rates & Inflation)—high yield found a ceiling in the mid 8% to 9% range (Figure 1). When yields are at these levels, the carry breakevens—the return buffer that current yields provide against further spread widening—become very attractive across a significant range of outcomes. This also helps explain why high yield assets, while not immune from the recent volatility, have held up considerably well relative to equity markets.

Figure 1: Yield to Worst for Global High Yield

Source: ICE BofA. As of April 16, 2025.

Source: ICE BofA. As of April 16, 2025.

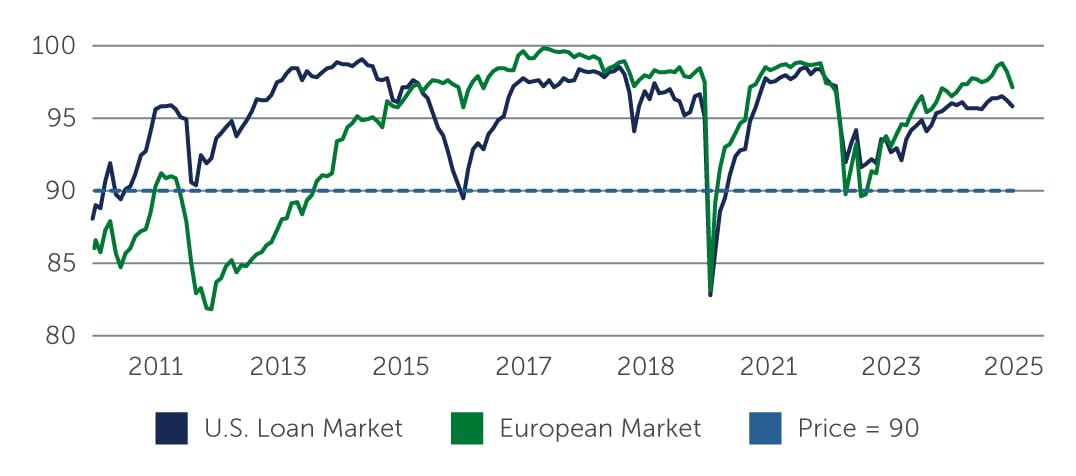

Similarly, in the loan market, elevated income provides ample support for performance, offsetting increases in spreads due to price declines and potential decreases in central banks' short-term rates. For context, with the average price for the global loan market around 95% of par, spreads would need to widen by 200 bps, remain at that level for an extended period, and be accompanied by a significant decline in short-term rates in the near term to push forward 12-month returns in the global loan market into negative territory. This scenario would place the average price in the high 80s, which typically requires a more substantial event—and, as shown in Figure 2, does not last long in most environments post the Global Financial Crisis.

Figure 2: Historical Average Loan Market Prices

Sources: Barings, S&P UBS Global Leveraged Loan Index. S&P UBS Leveraged Loan Index, S&P UBS Western European Leveraged Loan Index (non-USD). As of March 31, 2025.

Sources: Barings, S&P UBS Global Leveraged Loan Index. S&P UBS Leveraged Loan Index, S&P UBS Western European Leveraged Loan Index (non-USD). As of March 31, 2025.

Pockets of Opportunity

Going forward, given that periods of elevated yields for high yield bonds and discounted trading levels for loans are typically brief, we see advantages to building positions while maintaining some dry powder to capitalize on potential forced selling in the market should it arise. Financial markets often exhibit short-term pricing inefficiency during periods of dislocation or volatility. Considering the likelihood of further rallies and selloffs in the near to medium term, there is a case to be made for preserving cash balances to buy higher-quality credits that are trading down despite being largely sound from a fundamental perspective and unlikely to experience a massive disruption to earnings.

We also see the potential for opportunities outside of traditional high yield. Collateralized loan obligations (CLOs), for instance, can offer an opportunity to pick up meaningful incremental yield relative to traditional bonds and loans, and offer the added benefits of diversification and enhanced structural protection. In addition, should there be further selling pressure in the CLO secondary market as participants seek to raise cash ahead of volatility or to meet CLO ETF outflows, it could result in an attractive entry point and ultimately an opportunity to realize attractive risk-adjusted returns.

What’s Next: Positioning for Three “Likely” Scenarios

In light of the heightened geopolitical and macroeconomic uncertainty, it is difficult to have confidence in any one economic forecast. As our Multi Asset team mentioned in this recent article, there are three scenarios that seem most likely to unfold:

Scenario 1: The Trump administration’s tariffs are a negotiating tool that will be used to reach bilateral deals in the weeks/months ahead.

Scenario 2: The Trump administration believes so strongly in the power of tariffs—as a means of raising revenue and forcing manufacturing back into the U.S.—that it keeps them in place, regardless of near-term consequences.

Scenario 3: The prospect of economic contraction becomes painful enough that the Trump administration abandons its tariff programs.

While we are optimistic that cooler heads will prevail and the U.S. economy will see positive but slowing growth, there is a short-to-medium term risk that ongoing uncertainty could lead to sharp declines in business and consumer spending—and ultimately a period of slower growth or recession. However, even if prolonged tariff negotiations tip the global economy into recession, it’s worth noting that low growth and even mild recessions have not necessarily been bad environments for credit markets in the past. And most high yield issuers today, as mentioned, have the flexibility to continue to service their debt through a period of economic weakness, especially if that period proves to be somewhat mild and temporary.

The bottom line

The next few months will likely be turbulent. But volatility, while challenging, can also result in opportunities and attractive entry points for investors—especially when considering high yield’s sound fundamental backdrop, attractive breakevens, and margin of safety against default losses. That said, as the geopolitical and macroeconomic landscape evolves, active management and rigorous fundamental analysis will be key to navigating these uncertainties and capitalizing on emerging opportunities.

1. Source: UBS Neo. As of March 31, 2025.

2. Source: ICE BofA. As of March 31, 2025.

3. Source: ICE BofA. As of April 15, 2025.

4. Source: ICE BofA. As of April 15, 2025.