CLOs: 4 Factors to Watch

CLOs look well-positioned in the current environment, particularly given their floating-rate nature, robust structural protections, and potential for incremental yield—but risks remain on the horizon.

Collateralized loan obligations (CLOs) are coming off a strong couple of years. As a solid economic backdrop and attractive yields fueled demand for credit broadly, CLOs in particular stood out given the added benefits of a floating-rate coupon and robust structural protections. Returns, accordingly, have been strong across the capital structure. In 2024, AAA, AA and single-A CLOs returned 7.06%, 8.18%, and 9.25%, respectively, while BBB, BB and single-B CLOs returned 11.79%, 19.16%, and 36.72%.1

Can the strength continue? We believe it can, but there are unknowns ahead—particularly around the impact President Donald Trump’s second-term agenda could have on economic growth and rates. The CLO market, too, is in a different position than it was a year ago. Specifically, as is the case across credit more broadly, spreads are tighter and prices are higher, suggesting upside may be more limited going forward.

On the positive side, many of the tailwinds that powered the asset class over the last two years remain intact. While some are beginning to wane slightly, they will inevitably shape the market—and be worth monitoring—in the year ahead.

1. Improving Fundamentals, Manageable Defaults

Leveraged loan fundamentals continue to improve. Along with the 100 basis points (bps) of Federal Reserve (Fed) rate cuts in 2024, the significant repricing in loans last year—which helped push out maturities—have brought debt financing costs down. Continued moderation in rates, coupled with a solid economic backdrop, should help keep the default rate lower through 2025 and, similar to last year, we expect any forthcoming loan defaults to be largely idiosyncratic in nature.

A potential risk to this scenario is that inflation re-accelerates, which could at some point put rate hikes back on the table. While this is not our base case scenario, it is worth noting that CLOs have robust structural protections in place that can provide additional credit support in periods of stress. Accordingly, even in the event that the backdrop deteriorates slightly going forward and fundamentals become more stressed, we would not expect defaults to exceed the stress capacity that CLO structures were built to withstand.

2. Supply, Demand & The Rise of Retail

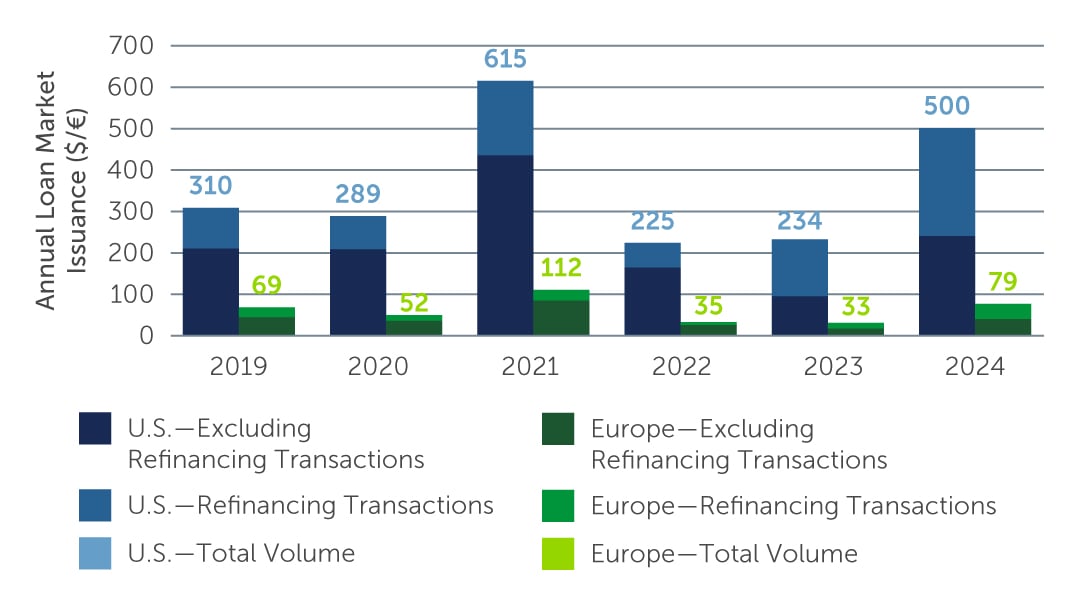

2025 is expected to be another year of heavy issuance, dominated once again by refinancings and resets as managers look to capitalize on tighter spreads and overall favorable market conditions (Figure 1). Pure CLO new issuance will depend on loan new issuance, which has been lackluster due in part to an increase in private market transactions. This loan issuance dynamic could begin to shift if M&A picks up more meaningfully on the back of lower rates.

The supply in the market continues to be met with strong demand, which we don’t see changing in the near term. In the top part of the capital structure, AAA buyers including U.S. and Japanese banks continue to lead the charge, although overall bank holdings came down slightly at the end of the year due to paydowns and amortizations. AAA CLO exchange traded funds (ETFs) have also seen substantial inflows, with CLO ETF AUM reaching $22 billion in 20242 and another $15 to $25 billion expected this year3. While this dynamic has generally been considered a positive, there are questions around what will happen if investors begin to pull cash from the funds going forward, particularly if rates fall and yields start to look less compelling.

For mezzanine tranches, demand persists from institutional clients that are drawn to the attractive carry on offer. Demand for BBBs in particular has been driven by buy-and-hold focused reinsurance buyers as they continue to grow and raise assets. There is also a significant amount of capacity sitting on the sidelines, much of it raised for multi asset credit strategies. Many of these strategies rely on BB CLOs for alpha generation but have been underweight in anticipation of a better entry point. If pockets of volatility—related to politics, rates or other factors—return to the market this year, demand will likely increase even from what we're already seeing, as the managers of these strategies look to deploy into the asset class opportunistically.

Figure 1: Refinancing Activity Dominates Issuance

Source: J.P. Morgan. As of December 31, 2024.

Source: J.P. Morgan. As of December 31, 2024.

3. Regulatory Changes

For higher-rated tranches, potential regulatory changes also look broadly supportive. Specifically, there is a proposed change to Basel III that would reduce the risk-weighted asset (RWA) requirement for AAA CLO tranches from 20% to 15%, effectively making it more attractive for U.S. banks to invest in these higher-rated CLOs. According to some estimates, this change could result in as much as $190 billion of excess capital entering the market in the next couple of years.4 At the same time, the NAIC—which is the main regulatory body for U.S. insurance companies—is revisiting the capital charge factors used in setting capital standards for certain asset classes, including CLOs. A recently published NAIC report suggests such a change would be supportive of demand for AAA, AA and single-A CLO tranches in particular.

4. Higher-for-Longer Rates

Although there is no shortage of views on the path ahead for interest rates over a longer-term horizon, most forecasts call for cuts to pause and for rates to remain relatively range-bound in the near term. In this scenario, coupons will come down slightly as well but remain high enough to drive continued demand for floating-rate assets like CLOs. Indeed, the floating-rate nature of CLOs means they are less sensitive, overall, to changes in interest rates compared to fixed rate debt—and with the 3-month term SOFR hovering around 4.3% and expected by many to remain around or above 4%, coupons should remain attractive.5 Yields, too, continue to look compelling in this environment, particularly in comparison to similarly rated investment grade and high yield corporate credit.

Not the Time to Take Unnecessary Risk

The backdrop for CLOs remains largely supportive, and we continue to see value across the capital structure. That said, most CLO tranches are trading close to par, and the basis between various profiles of deals and tranches has continued to compress. Accordingly—and given the many unknowns at play—we do not believe now is the time to take on additional risk, and our preference for quality and liquidity remains. AAA CLOs look particularly attractive from a risk-adjusted return perspective, and we expect them to continue to benefit from the positive technical backdrop and incremental spread potential relative to comparable fixed income products. For mezzanine tranches, all-in yields remain compelling, as mentioned, but discipline will be key given current spread levels and potential downside risks. CLO equity also presents an opportunity, in a continuation of the last several months. As still-strong underlying market conditions have continued to drive increased demand for CLO liabilities, liability pricing has become tighter, making the arbitrage for new issue equity particularly attractive.

And as always, a disciplined approach—together with careful, bottom-up credit and manager selection—will be crucial to selecting the right opportunities going forward.

1. Source: J.P. Morgan. As of December 31, 2024.

2. Source: Citi. As of November 26, 2024.

3. Source: Nomura. As of January 8, 2024.

4. Source: Morgan Stanley. As of December 2024.

5. Source: Bloomberg. As of January 2025.