Three Reasons to Consider European Real Estate Debt

The European real estate market is at the beginning of a new property cycle. Although the landscape is not devoid of risks, there are three key reasons why real estate debt presents a compelling investment opportunity—but a selective approach across sectors is crucial.

The recovery phase of the European real estate cycle has begun, with stabilizing prices paving the way for continued momentum in the coming years. Underpinning this positive backdrop, borrowing costs have eased and credit conditions continue to improve. Investor confidence has accordingly increased, resulting in more capital being deployed in the market. For commercial real estate (CRE) debt, these dynamics are giving rise to new loan origination opportunities that paint a bright picture for the asset class—especially when coupled with the ample refinancing opportunities ahead, given that €450 billion of debt matures over the next four years.1

Although the landscape is not devoid of risks, particularly as economic momentum cools in Europe and geopolitical risks rise around the globe, there are three reasons in particular that real estate debt presents a compelling opportunity:

- Significant downside protection potential

- Stable income profile and attractive return prospects relative to broader fixed income markets

- Exposure to structural themes such as changing demographics, e-commerce and ESG

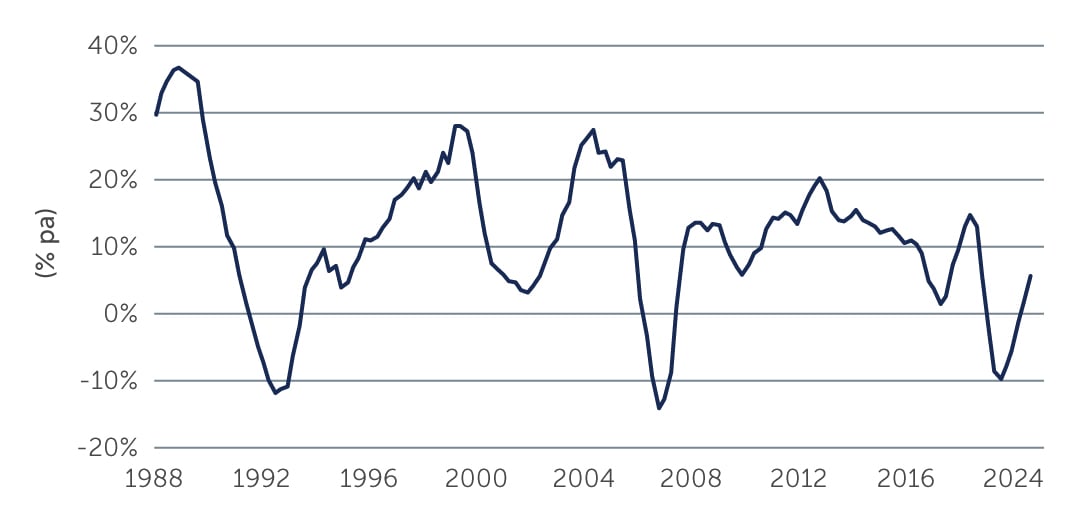

Figure 1: European All-Property Prime Total Returns

Source: CBRE, Cushman & Wakefield. As of Q3 2024.

Source: CBRE, Cushman & Wakefield. As of Q3 2024.

1. Source: Barings Research, MSCI. As of April 2024.