European Small Caps: Three Catalysts for Change

From changing interest rate expectations to potential political resolutions, there are reasons to believe that European smaller companies may be at a turning point.

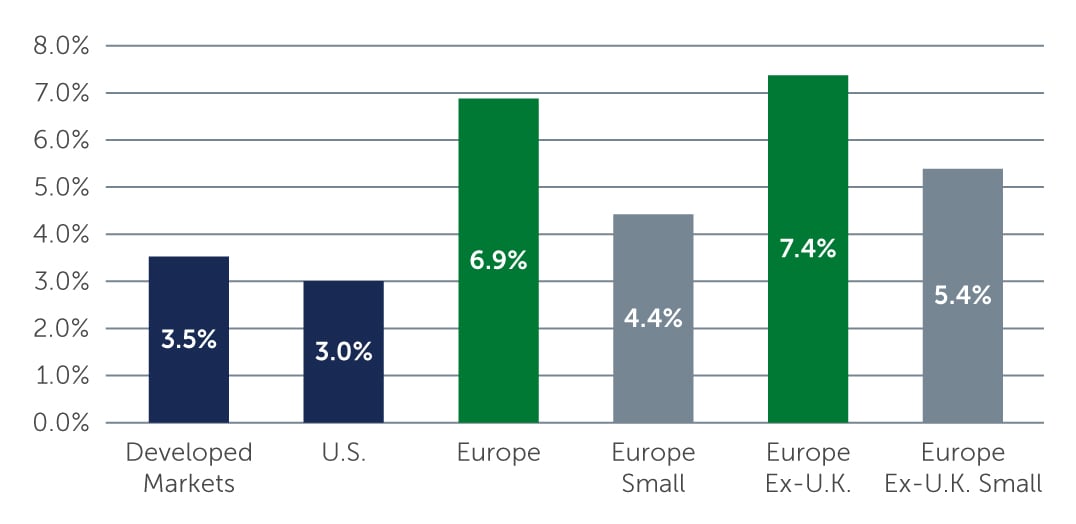

European equities have begun 2025 on a strong footing, outpacing both U.S. and broader developed markets this year (Figure 1). While this outperformance in part reflects both the recent decline in U.S. technology companies and a partial clawback of European equity indices’ relative underperformance since 2022, immediate concerns over trade tariffs have diminished.

Figure 1: European Equities Outperform Broader Markets YTD (US$)

Source: Barings, MSCI, Refinitiv. As of January 31, 2025. For illustrative purposes only. Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

Source: Barings, MSCI, Refinitiv. As of January 31, 2025. For illustrative purposes only. Any prediction, projection or forecast is not necessarily indicative of the future or likely performance.

In addition, relative valuations support this outperformance. In particular, even globally active and world-leading European companies are currently trading at substantial discounts to their U.S. counterparts.1 Meanwhile, smaller European companies, which have historically traded at a premium valuation compared to larger European companies, are currently valued on unprecedented discounts across both earnings-based and asset-related measures.2

Looking ahead, we believe there are three key themes that could shape a turning point for smaller companies across Europe.

1. Source: MSCI Europe Next 12 months PE Relative to MSCI U.S.A. As of January 31, 2025.

2. Source: MSCI. As of January 31, 2025.