High Yield: Shelter From the (Rate) Storm?

High yield bonds and loans have proven their ability to weather uncertainty and look well-suited for an environment in which rates, and potential rate volatility, may remain front-and-center.

Investors are facing a complex landscape to start the new year. In the U.S., much focus remains on President Donald Trump’s second-term agenda, specifically the wide range of potential policy outcomes and knock-on effects they could have on economic growth, inflation and interest rates. The U.S. Federal Reserve’s (Fed) response to these dynamics will be crucial, and is far from certain. While most market participants are calling for a continued moderation in rates going forward, particularly given the most recent inflation data, others are predicting no cuts for 2025. For those anticipating a second wave of inflation, there is a potential risk that rate increases may even be on the table—but it seems unlikely the Fed would pivot and raise rates, and it is not our base case scenario.

Despite this uncertainty, there are many reasons for optimism when it comes to high yield. For one, given the floating-rate nature of loans and the shorter duration of the high yield bond market today, total returns will be less impacted by any forthcoming rate volatility than may be the case for other asset classes. The solid fundamental and robust technical backdrop underpinning both U.S. and European high yield markets continue to be an anchor of support as well. And finally, the economic backdrop for the asset class remains broadly supportive. In the U.S., the economy still looks strong overall, although recent data has been mixed—jobs, for instance, have continued to surprise to the upside, while core CPI recently rose less than forecast, possibly turning the conversation more in favor of rate cuts. The European economy is more challenged, to be sure, with growth softer across a number of countries and the European Central Bank, accordingly, continuing on its path of rate cuts. But in our view, low or even modestly negative economic growth is unlikely to materially impede the return prospects for most European high yield issuers.

Together, these factors suggest that both high yield bonds and loans remain well-positioned and may be able to provide an effective shelter for weathering the months ahead.

Solid Fundamentals & A Higher-Quality Market

The fundamental picture for high yield issuers remains positive. Earnings are improving across most sectors, with the exception of certain cyclical industries, such as automotives and housing, that have been slower to recover amid still-elevated rates. Even if economic growth in the U.S. slows slightly going forward, that is not necessarily a bad thing for high yield issuers overall. What matters more, from a fundamental standpoint, is that we see some level of continued moderation in rates.

Across both the U.S. and Europe, many issuers have ample levels of liquidity and are in good financial health overall. For instance, net leverage and interest coverage in the U.S. are 3.6x and 4.2x, respectively, and 3.3x and 4.3x in Europe.1 Reflective of the healthy state of corporate fundamentals is the high credit quality of the market. Specifically, the percentage of BB issuers in the global high yield bond index remains near all-time highs at 56%, while the percentage of CCC and below issuers is around 11%.2 This higher-quality picture combined with solid fundamentals suggests that defaults are likely to stay within a manageable range going forward.

Locked-Up Capital is Stabilizing Demand

From a technical perspective, the strong tailwinds that prevailed in the high yield market through 2024 have persisted in recent months, with demand for both high yield bonds and loans continuing to meaningfully outpace supply. The low supply in the market is largely due to the continued absence of M&A activity. Although M&A is showing some signs of picking back up, with moderating rates likely to encourage further activity going forward, the technical backdrop should remain supportive in the coming months.

Interestingly, with regard to loans specifically, much of the strong demand is coming from locked-up capital, i.e., collateralized loan obligations (CLOs), or asset managers looking to create CLOs. This dynamic represents a departure from previous cycles, where demand was dominated by inflows/outflows from retail or broader institutional investors. While demand from CLO formation has typically been more prevalent in the European loan market, the theme is spreading to the U.S. market as well, and paves the way for more stability in demand going forward.

Loans: A Buffer Against Rate Volatility

In an environment mired with uncertainty, and with rate volatility likely to punctuate the months ahead, loans look particularly attractive. While loan defaults did increase last year—something that has garnered increased attention recently—it is worth noting that the majority of those defaults were priced into the market. Additionally, many defaults were concentrated among legacy issuers that had issued debt with high leverage in 2021, when rates were very low. Most of those challenged issuers have now gone through restructuring processes, such as liability management exercises (LMEs), and we expect defaults to come down this year as a result—particularly given that distress levels in the market are fairly benign against a backdrop of solid fundamentals and improving earnings growth.

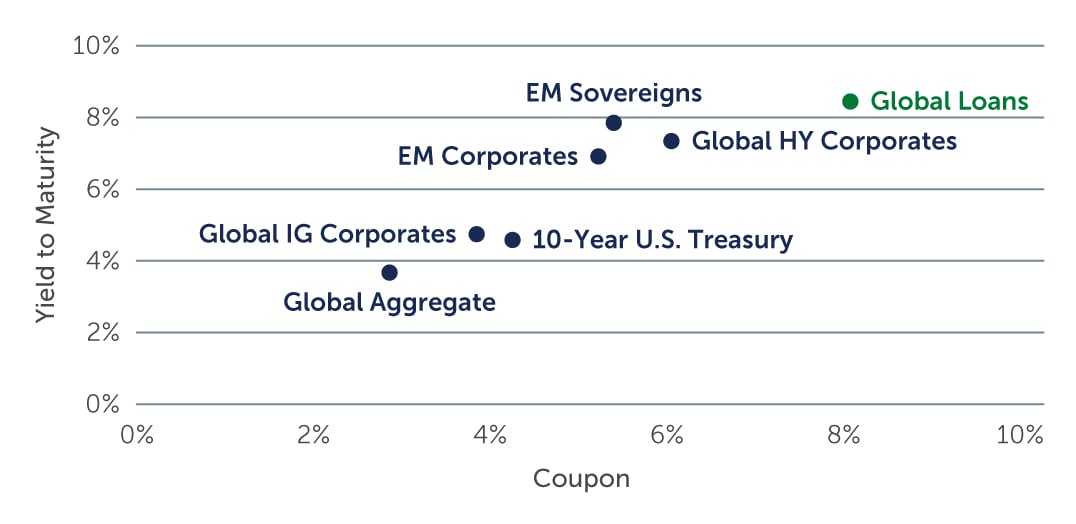

Going forward, the case for loans centers largely on the asset class’s floating-rate coupon, which means prices are less sensitive than fixed rate debt to changes in interest rates. Further rate cuts, if and when they occur, are likely to be measured, at least in the U.S., which suggests that loan coupons, which are around 8.3% in the U.S. market, should remain above historical averages (Figure 1). And notably, unlike other fixed income asset classes, the majority of the return on loans comes from contractual income that is being paid today rather than awaiting price recovery, which has resulted in a steadier return profile over time.

Figure 1: Loans Stand Out in the Current Environment

Source: Barings, Credit Suisse, ICE BofA, J.P. Morgan, Bloomberg. As of December 31, 2024.

Source: Barings, Credit Suisse, ICE BofA, J.P. Morgan, Bloomberg. As of December 31, 2024.

Bonds: The Benefits of Shorter Duration

There is also a case to make for bonds in the current environment, particularly against a backdrop of overall fundamental strength and, in the case of the U.S., a solid economy. The total return story remains compelling as bond yields continue to climb, with yields on BB and single-B bonds around 5.9% and 7.3%, respectively.3 The lower duration of the asset class is another key component of its value proposition. At just over three years, the average duration of the market suggests that bonds are more protected from interest rate swings than in the past. Another key attribute of the market is its callability. While spreads and yields-to-worst are calculated based on a bond’s legal maturity, most high yield companies refinance 12-24 months before that. Early calls can significantly impact total returns, adding as much as 50 to 100 basis points (bps) when bonds are trading at a discount to par, as they are currently.

Looking Ahead

The short duration of the high yield bond market and floating-rate nature of the loan market are indeed two of the key components to keep in mind while navigating the months ahead, particularly with rate uncertainty likely to remain front-and-center. Because of these characteristics, the impact of rate volatility on high yield’s potential total return profile in 2025 will likely be fairly minimal in the context of a broader asset allocation. And in fact, we saw this over the last three years, as return profiles for both high yield bonds and loans were strong both outright and relative to other asset classes.

Given that the market will likely remain well-supported from a fundamental and technical standpoint in the short to medium term, we believe both bonds and loans look well-positioned—even, and perhaps especially, against an uncertain backdrop. Of course, and as is always the case in uncertain times, rigorous analysis and careful, bottom-up credit selection will remain crucial to managing risks.

1. Source: CreditSights. As of September 30, 2024.

2. Source: Bank of America. As of December 31, 2024.

3. Source: Bank of America. As of December 31, 2024.