Developed APAC: A Compelling Growth Story

The Asia Pacific (APAC) direct lending landscape has undergone a considerable transformation over the past decade, particularly over the last four or five years. How does this change the middle market lending environment in APAC and what investment opportunity has emerged?

Rapidly Evolving Landscape

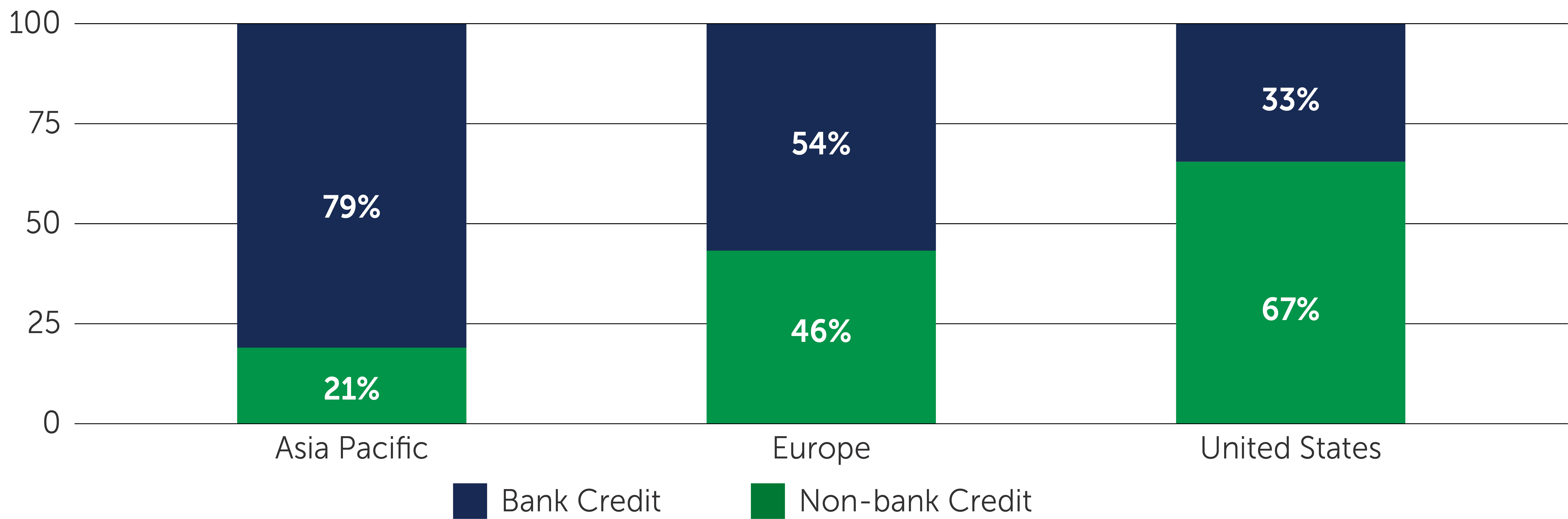

The Asia Pacific (APAC) direct lending landscape has undergone a considerable transformation over the past decade, particularly over the last four or five years. This evolution is partly due to the overall growth of the APAC middle market, which has accelerated the funding needs of APAC-based businesses. At the same time, banks—the traditional source of middle market funding—have been tightening their lending criteria and scaling back, similar to what we have seen in the U.S. and Europe. As a result, a new wave of institutional lenders has stepped in to fill the gap.

Figure 1: APAC Non-bank Lending Share Has Room to Grow

Source: Bank of International Settlements. As of December 31, 2023.

More international private equity sponsors have entered the APAC market as well. Accordingly, funds in the region—which historically tended to look primarily at special situations and opportunistic credit—are now looking increasingly toward traditional senior direct lending. In many cases, the sponsors have experience in the U.S. and European direct lending markets and are looking for the familiar benefits, like more flexible structures and speed and certainty of execution, that non-banks can offer. Managers that are part of a global platform can be at an advantage in this respect, often able to leverage their global relationships to directly originate opportunities in APAC.

Why Developed APAC?

There is a strong case to be made for focusing on the developed regions within APAC, such as Australia, New Zealand, Singapore and Hong Kong. These economies exhibit similar risk and return profiles as is typical of core direct lending strategies in the U.S. and Europe, with the added benefit of diversification and access to a compelling global growth opportunity. Importantly, the regulations and bankruptcy laws in these countries are comparable to those in other developed markets, meaning enforcement proceedings are reliable and transparent. Additionally, the sovereign credit ratings in these regions are similar to, and in some cases better than, those in the U.S. and Europe.

Through direct investments in developed APAC, it is also possible to gain indirect exposure to growth potential of emerging economies like China, India, and Indonesia—but with less idiosyncratic jurisdictional risk. In our view, these are currently less compelling regions from a senior secured direct lending perspective given the risks specifically around legal structures and enforcement of security.

Compelling Risk-Return Profile

The developed APAC direct lending market is still relatively nascent compared to the U.S. and Europe, but it offers similar risk and return characteristics. Because these regions are smaller in size and less developed from a capital markets perspective, while the middle market companies have similar EBITDA profiles (US$15 to US$100+ million), they tend to be first or second in their fields and have dominant market share. Leverage levels are generally consistent with transactions in the U.S. and European markets, if not slightly lower in some cases. Pricing tends to be less volatile as well, and documentation is relatively conservative.

While middle market companies in developed APAC have remained largely healthy, investors should also pay attention to sector selection. Companies in more defensive sectors, like education and health care, tend to exhibit more consistent corporate profits, higher cash flows and strong interest coverage. Demand tends to be less discretionary or price sensitive and therefore companies in these sectors are usually less impacted by changing economic conditions.

Why Now?

The current opportunity in APAC direct lending is rooted in the region’s growth story. In addition to benefitting from strong economic growth historically, demand for non-bank financing is strong—particularly in Australia and New Zealand—on the back of increased private equity activity from international and local PE sponsors.

The increase in non-bank lenders has also helped expand the breadth and depth of the direct lending market. Prior to the market’s growth both in size and number of deals, it arguably was not deep enough to build standalone diversified portfolios. But the landscape has evolved, and managers are also better-positioned to present private equity sponsors with more viable solutions, and to more meaningfully fill the gap left by banks. Investors’ appetite for direct lending has increased as well. As the narrative and understanding around these markets continues to grow, particularly among overseas sponsors and investors, we think the opportunity will persist.

24-3937132